My Investing Process

with two hats

Disclaimer: The information contained within this website and article is not financial advice and reflects my opinion in a strictly personal capacity. I am an engineer by training and profession; I do not possess formal qualifications in finance or investment. I may hold positions in the stocks mentioned and hence may be biased. This website and article aren’t written to give you advice. I am using it as my online journal to share knowledge and insights, and to gather feedback. I can’t guarantee the complete accuracy of all content, so please don’t rely on it. Please conduct your research or consult a professional financial advisor; I am not the one to provide this information.

When I first started buying shares, I had no process. I had read many books and blogs. I had listened to podcasts and watched videos. I soon learned that every investor has a different way to do this. There is no single correct method. That is fine in theory, but without a process, it is easy to buy for the wrong reasons and sell for the wrong reasons. I made those mistakes and upon reflection, I learned that the big wins are rare, the big mistakes are expensive. Avoiding those mistakes can put you ahead of most people. That realisation changed how I invest. One of the best ways to avoid mistakes is to follow a clear process. A process that is built around looking for risk first, then return

A process will not strike gold every time. It should not try to. What it can do is protect you from the worst decisions, the ones that hurt both the portfolio and the mind. In my view, that protection is often enough to beat the market over time. Fewer unforced errors, more time in the game.

This is simply my current process. It is not perfect, and neither am I. Even with a process, I still catch myself reacting to fear and greed. I am writing this in public to keep myself honest and to clear my own thinking, and to invite feedback. If something here helps you, great. If not, feel free to skip it.

Two hats on one head

As a retail investor, I play two roles. I am the Equity Analyst and I am the Portfolio Manager. It took me a few years to see the difference. Experienced investors often say these are separate skill sets. I agree. The challenge for a one-person shop is to keep the roles separate in practice.

Here is how I draw the line in my own work.

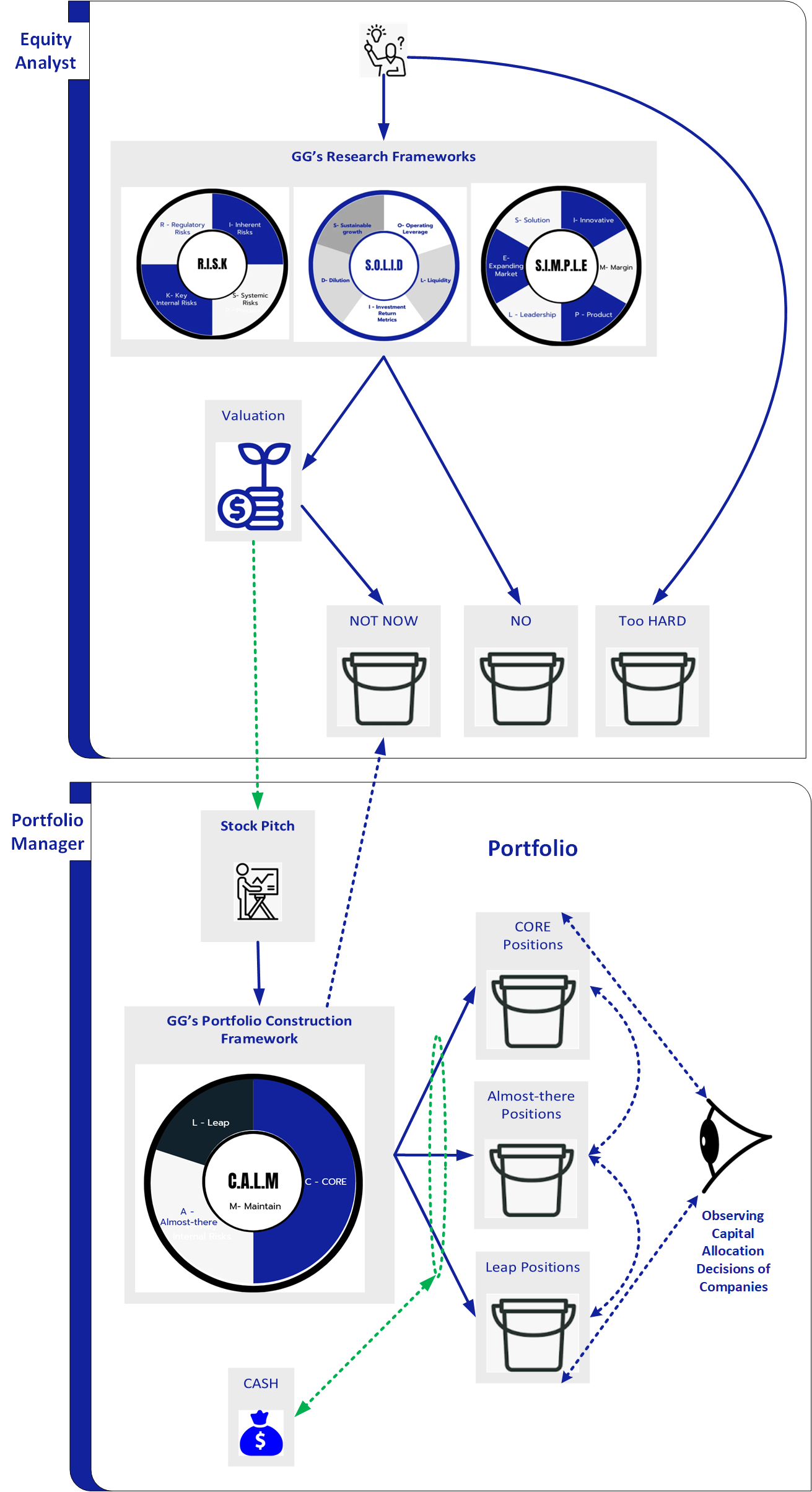

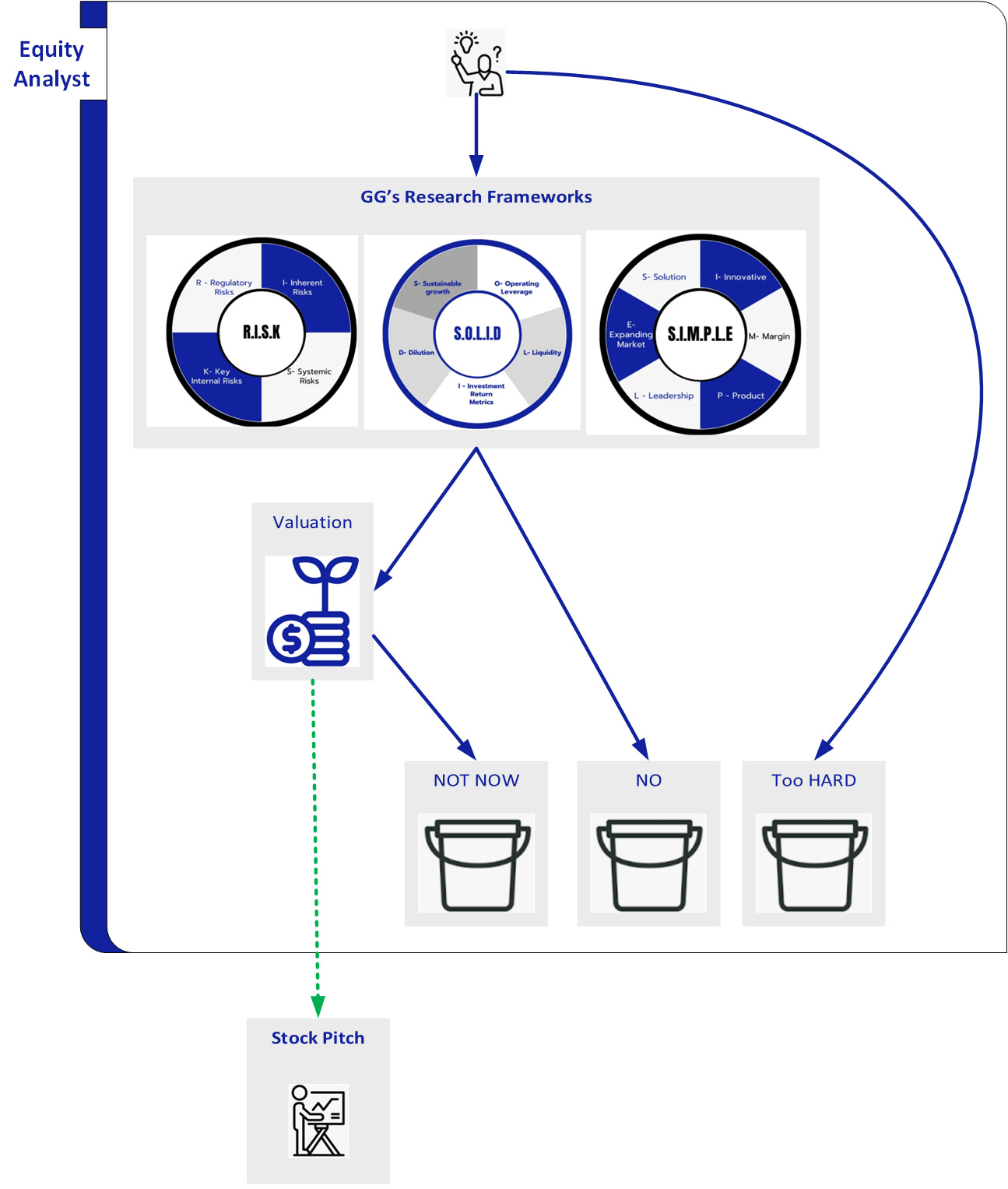

The Equity Analyst turns over rocks. This role studies many companies and decides which ones are inside my circle of competence. If a company passes that test, the analyst researches it, values it, and if it still looks interesting, prepares a short stock pitch. The analyst also monitors existing holdings to see if the thesis is on track.

The Portfolio Manager looks at the same company from a different angle. This role decides when to buy, how much to buy, and how the position fits with the rest of the portfolio. The manager also watches position sizes, risk, and cash.

I now ask myself a simple question before I act. Am I wearing the analyst hat or the manager hat? The following diagram shows my overall process.

So let’s delve a little deeper now

The Equity Analyst process

When a new company comes to my radar, I start with a simple filter. Do I understand how it makes money? Do I understand the product or service? Am I willing to follow this business for years? If the answer is no, the idea goes in the Too Hard basket. It is better to be honest than to pretend.

If the idea passes that first filter, I look at it from three angles. I have written about these before.

Qualitative Analysis using my SIMPLE framework. This covers the solution, innovation, margin, product, leadership, and size of the market.

Quantitative Analysis using my SOLID framework. This looks at growth, operating leverage, liquidity, returns on investment, and dilution.

Risk Analysis using my RISK framework. This lists regulatory, inherent, systemic, and key internal risks.

These frameworks are not magic. They are checklists that help me ask the same questions each time. If the answers look poor, the idea becomes a No.

If a company clears those checks, I try a simple valuation. I use free cash flow where I can. I use a range of growth rates rather than one precise number. I keep the math light and focus on the rough value zone.

If quality is fine but the price asks for perfection, it becomes Not Now.

If price and value line up, I write a short stock pitch. This is a few pages that explain the business, the thesis, the main risks, and what success might look like. The goal is clarity. The stock pitch is the hand-off to the Portfolio Manager.

The Portfolio Manager process

Now I change hats. I read the stock pitch like a stranger. I think about risk and reward. I think about how it fits with the rest of the portfolio. I also think about timing and position size.

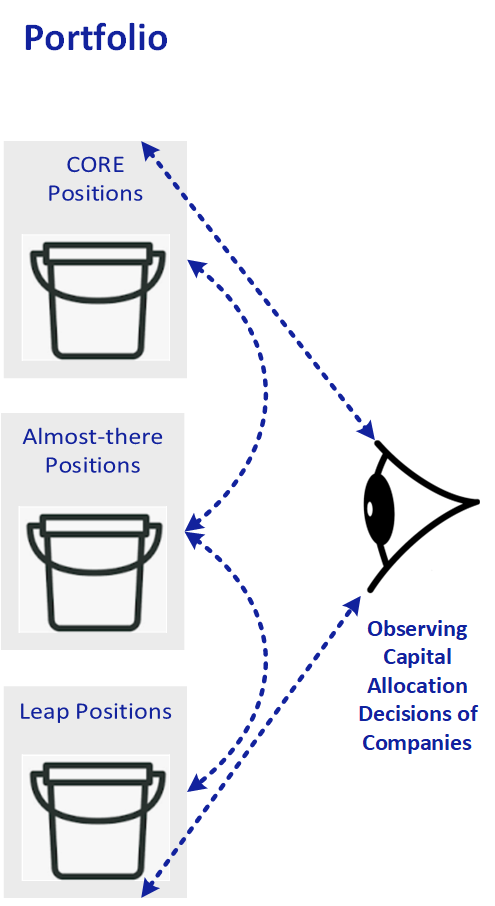

I use a simple portfolio construction framework I call C.A.L.M. I will publish a full piece on it sometime later. For now, here is the short version.

Core positions. These are proven compounders. They tend to sit around five percent.

Almost-there positions. These are solid but still maturing. They are often three percent.

Leap positions. These are earlier or catalyst driven. They are capped at two percent.

Companies can move between these groups as facts change. Alongside the buckets I keep a flexible cash sleeve. Cash rises when I cannot find good ideas at fair prices. Cash falls when the market offers value. There is no complex formula here. I make small adjustments and avoid big swings.

Ongoing monitoring

In the diagram, this sits under the Portfolio Manager, but in practice, both roles watch existing positions.

The Analyst watches the business. Are customers happy? Are returns holding up? Is the original thesis working? If facts change, I update the notes and the pitch.

The Manager watches the position. Is the weight still right? Has price run ahead of value. Does risk-reward still make sense given other choices? What are the tax and broker costs?

One area I pay special attention to is capital allocation. I look at how management spends its cash. Share buybacks. Dividends. Research and development. I wrote about it in my previous article.

Why does this help me?

A simple process does not guarantee good returns. It does help me avoid the worst mistakes. It gives me a calm path to follow when markets get loud. It creates a record I can review. When I get something wrong, I can see where the thinking broke and fix the framework.

This is my process today. It will not be my process forever. I expect to keep refining it as I learn. If you see gaps or better ways, I would love to hear them. The goal is steady progress, not perfection.

Great post. Thanks for the insights about your investing process. Would it be helpful to add in a process that identifies (once you’ve found a stock that deserves further research), which type of stock you are analysing/valuing i.e growth stock, value stock etc? I’ve seen one that the Brian’s from Longterm Mindset use which helps identify which part of the maturity cycle a particular business is in, which then informs the valuation method.